In 2026, banks and financial institutions in Saudi Arabia and the UAE are under increasing pressure to deliver faster, more personalized, and secure customer communication while strictly following SAMA and PDPL regulations.

Traditional channels like SMS, email, and call centers are becoming expensive and less effective. At the same time, customers now expect instant updates on their phones through the apps they already use daily.

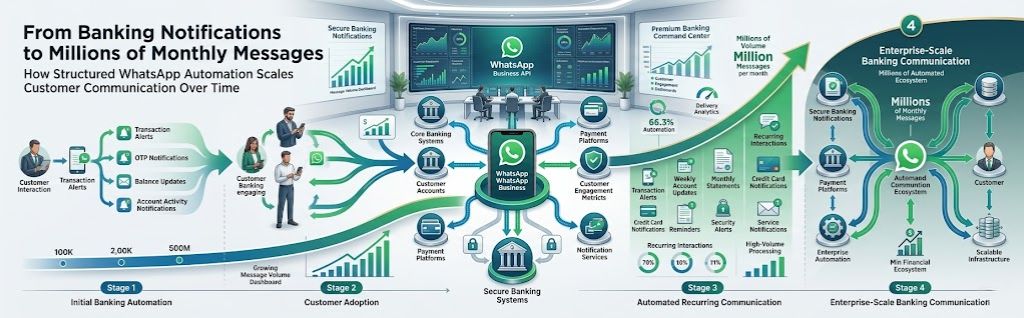

This is why many forward-thinking banks are moving toward structured WhatsApp automation powered by task-specific AI. When built correctly with proper compliance, this approach can handle high volumes of routine interactions while maintaining full regulatory control.

Why Banks in KSA & UAE Are Moving Toward WhatsApp Automation

Banks deal with very high volumes of recurring customer interactions every day:

- Balance inquiries

- Transaction alerts

- Payment reminders

- Loan and credit card status updates

- KYC and document requests

- Fraud alerts

- Statement delivery

These are mostly repetitive, rule-based interactions. When handled manually or through traditional channels, they create high operational costs and slower response times.

Structured WhatsApp automation allows banks to handle a large portion of these interactions automatically on a channel that customers already prefer, while keeping full control over the conversation flow.

Also Read About WhatsApp Mini-Apps & In-Chat Experiences for KSA & UAE Enterprises

Structured AI vs General Chatbots (Important Distinction)

Many banks are cautious about AI on WhatsApp because of compliance risks. The key difference lies in the approach:

- General/Open Chatbots: Risky for banking because conversations can go in any direction, making compliance difficult.

- Structured / Task-Specific AI Automation: Much safer and compliant. The AI is limited to specific, pre-defined tasks (e.g., balance check, mini-statement, payment status). This keeps conversations controlled and auditable.

This structured approach is what most serious banks in KSA and UAE are exploring in 2026.

Also Read About WhatsApp Chatbot for Travel Agencies

Real-World Use Cases in Banking

Example 1: Balance & Transaction Inquiries Customer sends “Balance” or “Last 5 transactions” → Structured AI responds instantly with accurate information from the core banking system → Conversation ends or offers next relevant action.

Example 2: Payment Reminders & Collections System automatically sends personalized payment reminders with secure payment links through WhatsApp. This has shown significantly higher response rates compared to SMS or email in many markets.

Example 3: Loan & Credit Card Status Updates Customers can check their loan status, upcoming EMI, or credit card due date directly through WhatsApp without calling the bank.

Example 4: Document & KYC Requests Bank can request documents through WhatsApp in a structured flow. Customer uploads documents directly in chat, which then goes into the bank’s system.

Example 5: Fraud & Security Alerts Real-time fraud alerts sent via WhatsApp with clear instructions. Because open rates on WhatsApp are much higher, customers are more likely to see and act on critical alerts quickly.

Also Read About How to Set Up Auto Reply on WhatsApp

Key Benefits Banks Are Seeing

- Significant reduction in inbound call volume for routine queries

- Faster response time to customers (seconds instead of minutes)

- Higher customer satisfaction due to 24/7 availability

- Lower cost per interaction compared to call centers

- Better compliance control through structured flows

- Potential for high recurring message volume (many banks handle millions of messages monthly)

Compliance Requirements (SAMA + PDPL)

For banks in Saudi Arabia, any WhatsApp solution must meet strict requirements from SAMA and PDPL. Key points include:

- Strong customer authentication for sensitive information

- Clear separation between service messages and marketing messages

- Full audit logs of all conversations

- Proper consent management

- Data must be handled according to PDPL requirements

- Solutions should preferably use sovereign or approved infrastructure

Only solutions designed with these requirements from the beginning are suitable for banking use cases.

Also Read About Top Bulk SMS Gateway Providers in Saudi Arabia for Businesses

Technical Architecture for Banking

A proper banking WhatsApp solution typically includes:

- WhatsApp Business API (Official)

- Structured AI / Flow engine (task-specific)

- Secure integration with Core Banking System

- Full audit logging and compliance reporting

- Data residency in approved jurisdictions

- Role-based access and encryption

Realistic Path to High Message Volume

Banks that implement structured WhatsApp automation at scale often see message volumes grow steadily. Because banking interactions are recurring (daily, weekly, monthly), once the system is live and customers start using it, message volume tends to increase over time.

Some banks in the region are already handling several million messages per month through WhatsApp after proper implementation.

Also Read About WhatsApp for Government, Smart Cities & Public Services in KSA

Who Should Consider This?

This solution is most relevant for:

- Banks and financial institutions in KSA and UAE

- Fintech companies

- Insurance companies

- Payment and fintech service providers

- Any financial organization handling high volumes of customer communication

Ready to Explore WhatsApp Structured AI Automation for Your Bank?

If you are looking to reduce operational costs, improve customer experience, and handle high volumes of communication in a compliant manner, structured WhatsApp automation is worth serious consideration in 2026.

FAQs

Q1: Can banks use WhatsApp for customer communication in KSA?

Many banks are exploring WhatsApp as a complementary channel when implemented with proper compliance.

Q2: What is the difference between structured AI and general chatbots in banking?

Structured AI is limited to specific tasks and flows, making it more controlled and suitable for regulated environments.

Q3: Is SAMA compliance required?

Yes. Any solution used by banks must align with SAMA guidelines.

Q4: Can WhatsApp help reduce call center volume?

Yes. Many routine queries can be handled through structured automation on WhatsApp.

Q5: Is it possible to reach high message volumes (millions per month)?

Yes, especially when multiple recurring services are automated.

Q6: How important is data security in banking WhatsApp projects?

It is critical. Solutions must follow strict security and data protection standards.

Q7: Can WhatsApp be integrated with core banking systems?

Yes. Integration is usually required for accurate and real-time responses.

Q8: What kind of interactions are suitable for WhatsApp in banking?

Balance inquiries, transaction alerts, payment reminders, status checks, and similar routine interactions work well.

Q9: How long does implementation usually take?

Timelines vary, but initial phases often take between 8 to 16 weeks.

Q10: Is WhatsApp suitable only for large banks?

It can be relevant for banks of different sizes depending on their customer communication volume and strategy.

Q11: Can customers initiate conversations on WhatsApp with the bank?

Yes, with proper setup and compliance controls.

Q12: What are the main compliance risks?

Risks arise mainly from poor data handling, lack of audit trails, or mixing promotional content with service messages.

Q13: Do you help with compliance documentation?

Yes. We support clients in designing solutions that align with regulatory requirements.

Q14: Can this solution work alongside existing channels (SMS, app, call center)?

Yes. WhatsApp usually works as a complementary channel, not a complete replacement.

Q15: How can we start exploring this for our bank?

We recommend beginning with a confidential discussion to understand your current systems, compliance requirements, and priority use cases.